There are many reasons to feel confident about our economic future in the US as of late. And why shouldn’t we feel this way? We have had a pretty bullish stock market run this year; the US and China appear to be reaching an agreement that will include a pullback on existing tariffs; earnings reports are coming in higher than expected; the unemployment rate remains at record lows; the Federal Reserve cut interest rates for a second time this year; and the new iPhone 11s are flying off the shelves just as the holiday season gets underway. So is a recession, let alone a great recession likely anytime soon? Yes. There are many problems at home and around the world that, if we choose to ignore, will lead to not only a US recession but a global recession, the next great recession. Here are just a few problems that can trigger it:

Speculative Bubble

Stocks with No Profitability

Stocks are overvalued. Many of these overvalued stocks continue to go up in value based purely on their lure of future gains and disruptive potential. And much like the IPO companies during the dot-com boom, many of today’s IPOs are overvalued and have no clear path toward profitability. Uber, for instance, has burned through nearly $2.6 billion in free cash flow in the past 12 months, a rate of $292,580 every hour. Although, Uber CEO Dara Khosrowshahi believes Uber has a clear path toward profitability by 2021, he failed to detail how Uber will achieve this. Instead, he focused on growth and expansion, all of which will require more spending.

An Overvalued Stock Market

Though many of these companies are considered “unicorns” because they are industry disruptors, “public market investors have become much more selective about which money-losing companies to back,” according to Polina Marinova in a Fortune newsletter dated September 30, 2019. It’s the reaction to what is all part of a speculative bubble that continues to grow as Wall Street ignores all of the signs of overvalued stocks coupled with a slowing economy.

Yale University professors Robert Shiller and John Campbell, explains the relation between overvalued stocks and financial collapses. Shiller’s Irrational Exuberance, published in March 2000 and titled after the then Chairman of the US Federal Reserve Allen Greenspan’s description of the US Stock Market, describes the commonalities between the 1929, 2000, and 2008 market crashes in relation to P/E and long-term interest rates. According to Shiller who received the 2013 Nobel Memorial Prize for Economic Science, we can historically see that the CAPE (Cyclically Adjusted Price-to-Earnings) Ratio, which is a 10 year average of P/E ratios, reached above 30 just before a significant financial collapse when long-term interest rates are low. This ratio is referred to as Shiller’s P/E Ratio. Shiller provided historical data dating as far back as the late 1800s.

The data shows that the CAPE ratio went above 30 August and September of 1929, just two months before the stock market crash of 1929 that resulted in the Great Depression. It again rose above 30 in 1997, peaking at 44.20 in December 1999 just before stock market crashed in March of 2000.

In September 2017, the CAPE ratio rose again above 30 and continues to fluctuate just above 30 since then. This could explain the amplitude in market volatility as we have seen several significant pullbacks since September of 2017 including the December 2018 losses.

Eventually, overvaluation is the key catalyst to total market collapse since what drives markets to overvalue stock is cheap credit and not higher earnings. A stock market crash similar to that of 1929, 2000 or 2008 would trigger a collapse a chain reaction whereby other bubbles would burst including many of the ones in this article, and this would result in the largest global economic recession in history.

Collapse of the Gig Economy

If companies like Uber go bankrupt, it can be devastating to our economy because Uber is part of the gig economy and one of the reasons the unemployment rate is so low. Uber, Lyft, HomeAdvisor, Etsy, Airbnb, Shopify, eBay, Amazon, Fiverr, Handy, Takl, HomeAway, Turo, UberEats, VRBO and hundreds of other online platforms that connect freelancers and small businesses to customers are all part of the larger gig economy. The gig economy is booming. About 53 million Americans are self-employed via the gig economy, enjoying flexible hours and additional income.

New policies, laws or depletion of investment funding, could disrupt or wipe out many of these platforms resulting in millions of people left without an income. New laws, like the one introduced in California requiring drivers of ride-hail companies to be classified as employees, will force companies like Lyft and Uber to employ rather than contract drivers. Drivers in California are divided because they will be forced into schedules that they cannot work with limited hours assigned to them so Uber and Lyft can avoid paying full-time benefits. This may force many drivers to leave. New Jersey is not far behind California, determined that Uber drivers are employees and calculating that Uber owes $30 billion for employment insurances.

Any disruption to the delicate, yet vastly unregulated gig economy would negatively impact our economy as a whole. Basically, everybody loses.

The Great Climate Retreat

A quiet migration is happening around the country. Entire communities are uprooting from areas that are prone to natural disasters caused by climate change and the government is paying for it. This is no surprise since the government is very much aware that climate change is real and that it is threatening our cities and towns. In fact, a government report from last year stated that climate change will increase the frequency of “powerful” storms.

When you tally the total cost of severe weather in the past 20 years including Hurricanes like Katrina, Irma, Maria, and Superstorm Sandy, the cost is in the hundreds of billions in destruction and disruption to our economy. Americans currently pay an average of $28 billion a year and it will increase to $39 billion annually by the year 2075. At least 6 major US cities are being threatened by climate change. All but one are coastal cities. Coastal cities make up 40% of all of the jobs in the US and 46% of US GDP.

The cost to replace entire communities every time there is a severe storm is becoming too expensive. For this reason, the government started buying out homes in flood prone areas. They are calling this the Great Climate Retreat. From Staten Island, New York to Marathon Florida, and from Houston, Texas to New Orleans, Louisiana, local governments are coordinating the buyout of homes in flood prone areas. According to Claims Journal, a journal dedicated to insurance, 13 million Americans will be forced to move away from coastal areas due to rising sea levels at an average cost of $1 million per home by the end of the century.

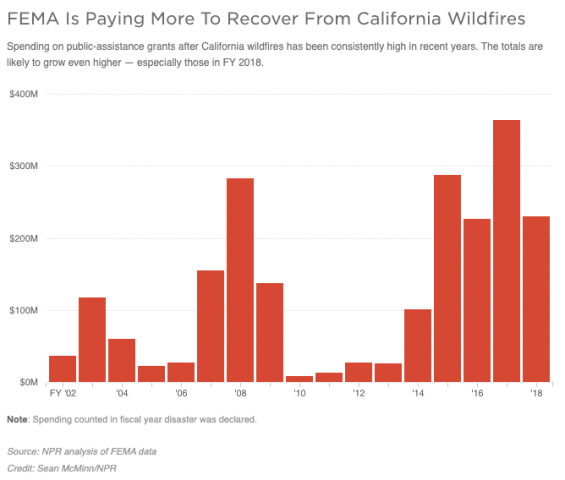

One year after the deadly Camp Fire wildfire destroyed the entire town of Paradise, California residents are still displaced. At a cost of $16 billion, the Camp Fire wildfire was the “most expensive disaster in the world in 2018,” according to Kirk Siegler of NPR.org. Longer than usual droughts and higher than usual sustained winds believed to be caused by climate change are to blame for the record number of wildfires in California in recent years. Taxpayers are paying the rising costs associated with these destructive wildfires.

All of the cities mentioned are experiencing record heatwaves, but no city is feeling it more than Phoenix. Nearly half of the year, Phoenix experiences temperatures above 100 degrees and if temperatures continue to rise at the current rate, the city will be uninhabitable by 2050.

Morgan Stanley estimates the cost of climate-change related weather to be $415 billion in North America in the last three years. Much of it is due to wildfires and hurricanes. The cost of living and the cost of disaster recovery in disaster-plagued communities have forced tens of thousands of families to migrate and this will only continue to increase. This is in addition to the tens of thousands of people who were already displaced who decided not to return and build in disaster-prone communities.

China

A failing Chinese economy would not be good for the US or any other country. Though the US economy suffers from trade deficits caused by unfair trade practices on the part of China, a total collapse of the Chinese economy will certainly lead to a US and possibly, worldwide economic collapse.

Trade Wars

The current US-China trade war is not only adversely affecting the US and Chinese economies, they are affecting the economies of our other trade partners. Australia, for example, accounts for 33% of its exports to China making China its largest trade partner. Germany, Japan, and South Korea are also major exporters to China. The US is the number one exporter to China of semiconductors, automobiles, aircraft, and soybeans. The US is also the second-largest exporter of building materials to China. According to data published by Export.gov, 13% of building materials that China imports come from the US. These are major US industries that rely heavily on China. Tariffs imposed on Chinese imports is already affecting the Chinese economy. To add wood to the fire, China’s attempt at retaliation by imposing its own tariffs will only speed up the collapse of an already fragile Chinese economy. The US and its other trade partners have economic interests that will affect their exports should the Chinese economy collapse.

Housing Bubble

China just keeps borrowing and spending and there is a reason for this. Local Chinese governments only receive 40% of tax revenue, yet they are responsible for 80% of local expenses. To generate additional revenue, local governments buy cheap rural land, then they rezone the land for city development and then they sell the newly rezoned land for a much higher price to developers. The developers, who are either state-owned or privately owned develop buildings and then sell them. There is a high demand for property in China and there is a reason for this too. Thanks to China’s one child policy there are now more men than women in China, making the search for a wife more competitive. Real estate is regarded as the highest level of financial security. If a man does not own property, chances are slim he will marry, and because of this, entire families will pool money together to help them buy property. The problem is that entire new ghost cities keep popping up in isolated rural areas and since these cities are not located near any jobs people are buying up the properties but no one is living in them. The most famous of these ghost cities is Ordos City which boasts modern architecture, yet it remains largely empty.

The Chinese government is spending billions on new bullet train railways and millions of dollars in incentives to bring foreign businesses to these ghost cities. Local governments will continue to do this because it is the only way for them to generate money and fuel local economies so that the local politicians are viewed favorably by the Chinese central government. This has caused a housing bubble that is not sustainable. Eventually, the demand for new housing will decrease. Currently, there are nearly 64 million unoccupied homes in China that currently hold a mortgage balance, most of which are located in ghost cities. For now this vicious cycle continues, however, Australia, one of China’s main exporters of iron for construction, is beginning to see a slowdown.

Increasing Debt

China’s debt is far greater than China’s GDP. As of last December, the total debt was 50.5% of the total $13.6 trillion GDP. China’s total debt from corporate, household and government borrowing is over $40 trillion, 303% of China’s GDP according to the Institution of International Finance, as reported by Reuters.

The debt to GDP ratio is only getting worse as the GDP is growing at its slowest pace in 27 years. The western world is already beginning to blacklist most of China’s technology products over concerns that the Chinese government is spying on western countries. One can make the argument that China’s economy is nearing a total collapse as the debt continues to increase and GDP begins to decline.

To make matters even worse, worldwide, Chinese companies make up about 27% of all of these emerging markets according to Barrons. Forbes sites that China represents 38% of the total market capitalization of emerging markets. In short, if China’s economy collapse, it will send the world into an economic crisis.

Negative Interest Rate Policies (NIRP)

Though Japan and the European Central Bank were not the first to experiment with negative interest rate policies (NIRP) to jumpstart their economies, it did not become the topic of daily discussion here in the US until Trump became critical of the US Federal Reserve for not implementing the same policies.

Why doesn’t the Federal Reserve adopt a NIRP? To understand why we need to understand how NIRP works. To do this, we first need to understand the relationship between central banks and banking institutions. In the US, our central bank is the US Federal Reserve and the banking institutions, or banks, are the institutions where people like you and I keep our savings and checking accounts. When we talk about Federal Reserve interest rates, it is in relation to what the Federal Reserve pays in interest to banks for holding the banks’ money on deposit at Federal Reserve banks. Negative interest rates means that this relationship is inverted. Instead of the Federal Reserve paying interest for these same deposits, the banks pay the Federal Reserve. Hence the term negative interest. It does not mean banks will pay you interest for having a mortgage with them.

So, what does it mean? What it does mean is that banks will either pass the interest fees on to their customers. It also means is that banks will look for other ways to make their money work because are in the business of making money from interest on loans. So, they will give out more loans and more freely, meaning with less scrutiny of the borrowers’ ability to pay back the loans. This, in turn, will encourage more people who are less qualified to take out loans to obtain mortgages at lower interest rates and this will lead to higher home prices and a new real estate bubble. This is what caused the Financial Crisis of 2008 which, according to Former Federal Reserve Chair Ben Bernanke, “was the worst financial crisis in global history, including the Great Depression” of 1929. Even if no mortgages default, the rising cost of real estate alone will have a negative impact on everyone from residential to commercial leasing because landlords need to charge higher rents to cover the higher mortgage balances. NIRP would only compound the affects of an economic slowdown caused by leveraged debt because a NIRP also discourages people from having any savings and checking accounts from all the bank fees that would result from a NIRP.

Though the US Federal Reserve is not planning to adopt a NIRP, regardless of the President’s position on negative interest rates, the US is still exposed to the economic threat to banks in other countries that have adopted NIRP. Germany’s Deutsche Bank is beginning to show stress cracks. Deutsche Bank’s president Carl von Rohr stated in a speech on November 6, 2019 that negative bond yields will push the European Union into an economic recession and banks will not be able to survive. NIRP are quite possibly the most immediate threat to the global economy.

Insolvent Pension Plans

The most common type of pension plan for civil servants is a Defined Benefit Plan (DBP). Unlike typical employer sponsored retirement plans like 401K plans, which are structured based on the defined contributions, DBPs are structured based on the defined benefit to be distributed at retirement. DBPs require employers to cover a specific return each year. Typical DBPs require annual returns between 7% and 8%. Unfortunately, only twice since 1871 did 50% of all DBPs in the US achieved returns of 7% or higher year over year. This has created a pension fund shortfall that continues to widen. Pension Benefit Guaranty Corporation (PBGC), an insurance plan established by the US government to takes over failed pension plans from bankrupted single companies and multi-employer industries, projects that their multi-employer insurance program will become insolvent by the year 2025.

Underfunded pension plans are not only a US problem but a worldwide problem. Currently in the US, the total underfunded dollar amount across all pension funds is roughly $6 trillion. The figure is upwards of $70 trillion across 8 countries, Japan, Australia, Netherlands, India, China, United Kingdom, United States, and Canada. With a daily increase of $24 billion per day, the pension gap in the US will reach $38 trillion and $400 trillion worldwide by 2050.

Retiring Baby Boomers

Baby Boomers are entering retirement age. This means that Baby Boomers will eventually be cashing in their retirement funds, downsizing their homes and spending less.

Baby Boomers make up 36% of the nearly one trillion dollars invested in target-fund retirement accounts, which are designed to adjust risk exposure as retirement account investors advance closer to the target retirement age. Since there is greater risk in equity positions as opposed to fixed income positions, there will be a steady outflow of investment capital in equity markets. As Baby Boomers retire, there will be a steady withdrawal out of markets as a whole. But it’s not just the stock market. This is spilling over into the real estate market. As retired Baby Boomers look to downsize, there just aren’t enough people looking to buy real estate. There isn’t enough new investment capital from younger generations to make up the difference. According to a 2017 BlackRock survey, Millennials are holding on to cash more than any other prior generation.

Student Loans

In the US, federally backed student loans have surpassed $1.6 trillion according to the Washington Post. Student loan debt is at 7.59% of the total national income. This drag on todays workforce, particularly the workforce entering just after graduating from college and from post graduate degree programs. Not only are they entering the workforce later in life, they are also more likely to put off starting a small business, buying a home, invest or starting a family. This is because they have huge student loans to pay off after graduation, leaving them with little money to do anything else. According to one source the average college graduate has a negative cash flow of $4,000 a year. Student loans are also forcing people to find roommates to share monthly expenses. As many as 38% are living with their parents, postponing getting their own place indefinitely. Many parents, who themselves have mortgage obligations and multiple children attending or graduating college also have to co-sign many of these loans.

As more people graduate and enter the workforce, the less number of jobs are available. As a result, more people are relying on the gig economy, not only for additional income, but also to help offset the monthly cost of student debt.

The student loan debt is increasing at an alarming rate. The ratio of student debt to national income has nearly doubled since the mid-2000s. It is creating barriers towards investing and future borrowing. With little or no assets to leverage against debt, any weakening in employment levels will have a considerable impact on student loan repayment. According to Alexander Tanzi, the US student loan debt in serious delinquency tops at $166 billions. As more people take on new federally backed student loans, the probability of loan defaults will continue to increase. This will have the same ripple effect on the US economy that the federally backed mortgage defaults had on the US economy back in 2008, sending the US economy into another recession.

Though I’ve highlighted why many of the problems we face can lead us to another recession, a great recession is less likely. The world economy is more stable today that it was in 2008 and during prior recessions. The fact is that many factors have to be considered to predict the next great recession. Political turmoil, trade wars and unstable governments also play a role in the world economy. None of these factors were mentioned here and should be considered.

All of the problems mentioned here lack one commonality, sustainability. That is the root of all economic bubbles, the lack of sustainability. Governments should focus their efforts less on stimulating economic growth and more on achieving finding sustainable balance because history has shown us that growth is not always sustainable. Eventually, every growth story includes a correction period. The struggling middle and lower-middle classes in every society are the ones who are hurt the most during these correction periods. This may be why the US Federal Reserve won’t consider negative interest rates. Maybe it’s because it is unsustainable and the US Federal Reserve decided they just don’t want to hurt the people of this great country.

Thanks for this amazing information